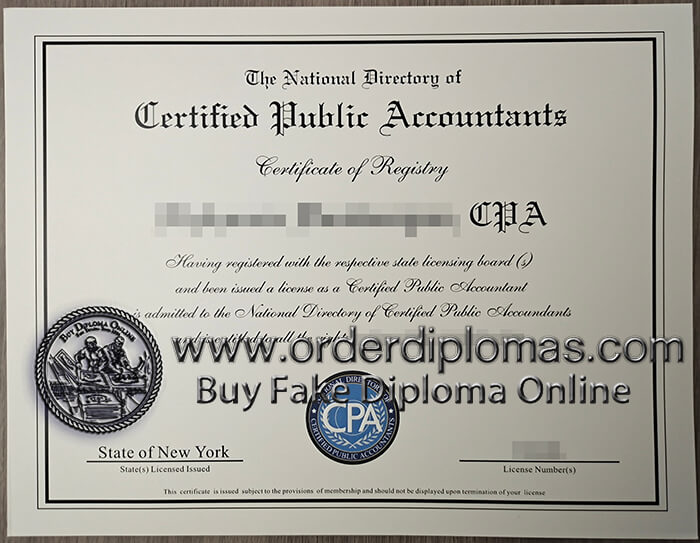

buy fake state of new york CPA certificate

How to buy a fake state of new york CPA diploma? how to buy a fake state of new york CPA degree? how to buy a fake state of new york CPA certificate? buy fake state of new york CPA diploma. buy fake state of new york CPA certificate. buy fake diploma. buy fake degree. buy fake certificate.

PREAMBLE

The following, as amended from time to time, shall constitute the bylaws of NEW YORK STATE SOCIETY OF CERTIFIED PUBLIC ACCOUNTANTS (hereinafter the “Society”). The Society has been organized and shall exist as a nonprofit corporation pursuant to its Articles of Incorporation and the New York Consolidated Laws, Not-For-Profit Corporation Law (the Act). Notwithstanding the foregoing, the Society shall be operated at all times as a 501(c)(6) organization within the meaning of the U.S. Internal Revenue Code of 1986 as amended from time to time (the “Code”) and the activities of the Corporation shall be limited accordingly.

.

ARTICLE I — OFFICES; PURPOSE

1. Principal Office—The principal office of the New York State Society of Certified Public Accountants, a New York nonprofit corporation (hereinafter referred to as the “Society”), shall be located in New York, New York. The Society may relocate the principal office, and may also establish such other offices, as the Board of Directors shall direct if the business of the Society so requires.

2. Registered Office and Agent—The Society shall maintain a registered office and a registered agent within the State of New York in accordance with the requirements of the Act. The location of the registered office and the designation of the registered agent shall be approved by the Board of Directors.

3. Nonprofit Purpose—The Society is a nonprofit corporation and is not organized for the private gain of any person. It is organized under the New York Consolidated Laws, Not-For-Profit Corporation Law and is organized for the purposes set forth in Internal Revenue Code section 501(c)(6) or the corresponding provision of any future United States internal revenue law. Within the context of these general purposes, the Society’s specific purposes shall be to serve as an advocate and resource for Certified Public Accountants by representing and cultivating the profession’s core values of integrity, professionalism, and ethics. Notwithstanding any other provision in these bylaws, the Society shall not, except to an insubstantial degree, engage in any activities or exercise any powers that do not further the purpose of this Society, and the Society shall not carry on any other activities not permitted to be carried on by a corporation exempt from federal income tax under Internal Revenue Code section 501(c)(6) or the corresponding provision of any future United States internal revenue law.

4. Dedication of Property—

(a) All corporate property is irrevocably dedicated to the purposes set forth in Article I, Section 3. No part of the net earnings of the Society shall inure to the benefit of any of its directors, trustees, officers, or members, or to the benefit of any private person except as reasonable compensation for services rendered, goods received, and other property or valuable thing which may be acquired by the Society for the accomplishment of its purposes.

(b) On the winding up and dissolution of the Society, after paying or adequately providing for the debts, obligations and liabilities of the Society, the remaining assets of the Society shall be distributed to nonprofit funds, foundations or corporations which have established their tax-exempt status under Internal Revenue Code sections 501(c)(3) or 501(c)(6), or the corresponding provision of any future United States internal revenue law, and which have their principal area of activities in the State of New York and which have as their principal purpose the cultivating the Certified Public Accounting profession’s core values of integrity, professionalism, and ethics.

Top of Page

ARTICLE II — MEMBERSHIP

1. Classes of membership—Membership in the Society shall consist of two classes: CPA members and associate members. As used in these bylaws, the term “member” shall refer to any member unless the context clearly indicates a member in a specific membership class or category.

2. CPA members—Any person who is licensed as a certified public accountant (“CPA”) in good standing of New York State or any other state or political subdivision of the United States (“U.S. Jurisdiction”) shall be eligible to apply to become a CPA member of the Society.

3. Associate members—

(a) A person who is not a CPA and meets the requirements of one or more of the following categories shall be eligible to apply to become an associate member of the Society.

(1) International associate. A person who (i) holds a CPA certificate issued outside a U.S. Jurisdiction or is a chartered accountant and (ii) is a member in good standing of an association belonging to the International Federation of Accountants shall be eligible to apply for membership as an international associate.

USA Diplomas

USA Diplomas Canada Diplomas

Canada Diplomas UK Diplomas

UK Diplomas Australia Diplomas

Australia Diplomas Germany Diplomas

Germany Diplomas Malaysia Diplomas

Malaysia Diplomas Singapore Diplomas

Singapore Diplomas Other countries

Other countries Transcript-Form.xlsx

Transcript-Form.xlsx